Unlocking Capital Support for Pet Lines Growth

Author: Andrew Hellman (Stride Systems)

Pet insurance loss ratios run roughly 14 points above the personal lines average. Approximately half of that spread reflects veterinary cost inflation; the remainder reflects an addressable behavioral data gap. Closing that gap unlocks capital support confidence for one of the fastest-growing lines in property and casualty.

Pet insurance is one of the fastest-growing lines in global P&C. The industry expects premiums to climb from roughly $20 billion in 2025 to $80 billion by 2033 [1]. Growth at that rate needs capital to scale, and capital stands behind a risk only when that risk can be priced with confidence. Pet lines cannot yet be priced with that confidence. Loss ratios run roughly 14 points above the personal lines average [2] [3], and they have held there for years rather than converging the way a maturing line should.

Insurers currently price pet policies by modeling a highly dynamic behavioral risk using static inception factors such as breed, age, location, and perhaps a cursory medical or claims history. The behavior that actually drives the claim, how consistent the routines are, how early care is sought, how well the environment fits the animal, how stable daily life is, is never observed. This is the behavioral data gap. It is the other half of the spread, roughly 7 points and $20B through 2033 (cumulative), once the frequently cited effect of veterinary cost inflation is set aside.

A loss that cannot be observed cannot be estimated with precision, and a loss that cannot be estimated cannot be priced with confidence. Capital will temporarily carry a high loss ratio that it can understand, on the expectation of normalization over time, because a foreseeable loss can be baked into the premium. It will not commit fully to a fast-growing line without the rational expectation of a defensible return against competing alternatives. The cautious capital and the expected growth are therefore locked together, each holding the other back. The market will reach its projected size only when the risk beneath it can be accurately assessed and priced accordingly.

The remedy follows directly from the diagnosis. A data gap that exists because an input is missing closes when that input is supplied. In this case, that input is longitudinal behavioral data (“LBD”): the animal-human pair observed continuously over time, rather than captured once at inception or instrumented without regard for the determining human context. Supplied at scale, LBD renders the dynamic risk legible, the loss estimable, and the line priceable with the confidence capital requires. Further detail of what this data must observe and how it must be made ready for ingestion into advanced analytics environments is provided in the white paper Pet Insurance Loss Ratios: Addressing the Behavioral Data Gap.

To maximize effectivity, the scope of LBD is intentionally limited. Pet lines is overwhelmingly a dog business, and that is where the problem is both largest and most solvable. Two reasons converge. The first is scale: dogs are roughly 80% of pet lines premiums [4], so to solve the dog book is to solve most of the line. The second is observability: a dog's risk runs through its uniquely legible relationship with the human household, which unlike other pets produces well-documented behavioral patterns linked to breed-type instinctive drive and human household context, both recurrent and measurable over time.

The problem is therefore narrower than it looks. Solve for the dog, and the most addressable portion of the loss ratio gap is meaningfully remediated, after which capital will logically follow.

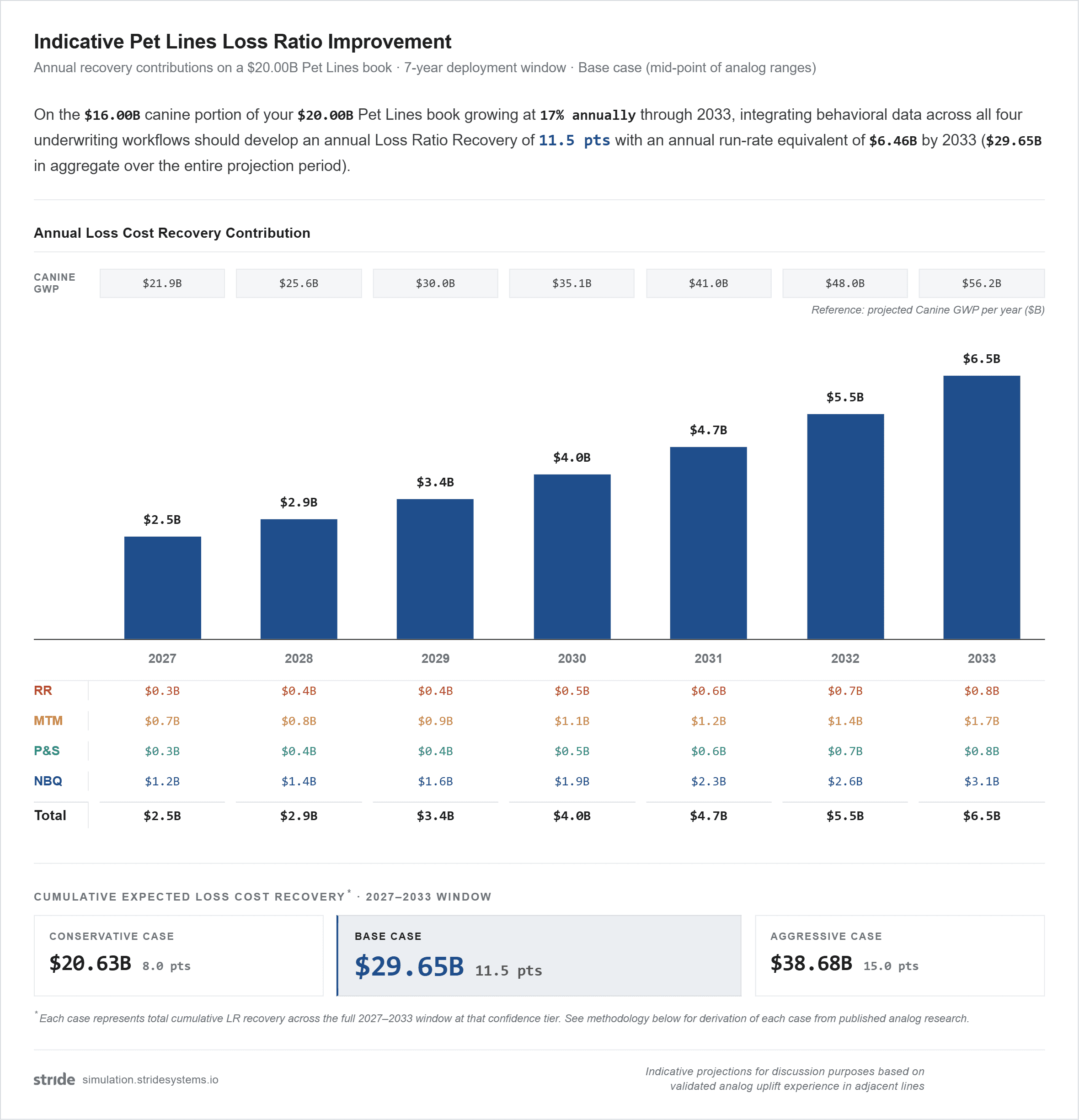

The size of the opportunity has already been measured. A companion piece in this series, The Recoverable Value of the Pet Lines Loss Ratio Gap, puts the cumulative recoverable loss cost for the dog portion of the global pet book, on industry GWP projections for 2027 to 2033 [5], at $29.7 billion in the base case and $20.6 to $38.7 billion in the conservative and aggressive cases, respectively. For the underwriter, this is recovered loss cost; for the capital provider, it is restored margin which unlocks incremental capital to support growth. The industry has funded the analytics heavily. The gating constraint is not analytical capacity. It is the absence of the input to feed it: a measure of the longitudinal, behavioral risk between policy inception and claims events.

———

Stride Loss Ratio Recovery Simulation, global pet lines book, 2027 to 2033. Model your own book at simulation.stridesystems.io.

———

The same gap costs the line in two further ways worth noting, each flowing from the same failure to measure the determinant underlying behavioral risk. Priced with a wide margin for unpredictable claims variance, the product stays expensive, and penetration in the United States, the largest pet lines market, sits near 4% [6] against unambiguous demand across the wider pet wellness category. And because insurance has historically priced the predictable layer of pet care too fully given wider loss dynamics, it is beginning to lose competitive position to veterinary group wellness subscription plans designed to cover the low-variance vaccine and maintenance costs. Were this shift to accelerate, the insurer would be left with the tail accident and illness claims that are hardest to price and least rewarding to hold. Each is the same problem in another form. A line that cannot see its own risk prices it poorly and surrenders ground it should hold. Markets route around mispricing.

None of this is a new theory. It is the plain consequence of a gap the industry has tolerated only because the problem appears outside direct control (systemic vet cost increases), or simply intractable (LBD). The data that would close it does not yet exist at the scale this requires. Assembling it is a substantial undertaking, and that perceived difficulty is the reason it remains unsolved, not a reason it cannot be. The apparent difficulty notwithstanding, the logic admits little argument: capital follows confident pricing, confident pricing follows longitudinal behavioral data for dynamic human-determinant systems, and the underwriter that accesses that data first is the underwriter that capital will back.

The work now underway at Stride Systems is the building of that behavioral data input for pet lines analytics. The full analysis, including how the addressable half of the gap is sized against the global dog book, is set out in the white paper Pet Insurance Loss Ratios: Addressing the Behavioral Data Gap, with an interactive Simulation that models the recovery logic derived from canonical loss ratio uplift using analogs in adjacent lines applied to a participating pet lines book.

- -

Stride Systems builds longitudinal behavioral data infrastructure for pet lines underwriting.

For further discussion, contact andrew@stridesystems.io.